Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2026 | 29 Posts

- 2025 | 49 Posts

- 2024 | 50 Posts

- 2023 | 36 Posts

- 2022 | 53 Posts

- 2021 | 63 Posts

- 2020 | 77 Posts

- 2019 | 1 Posts

- 2018 | 2 Posts

- 2016 | 3 Posts

- 2015 | 8 Posts

- 2014 | 1 Posts

- 2012 | 1 Posts

- 2011 | 2 Posts

11

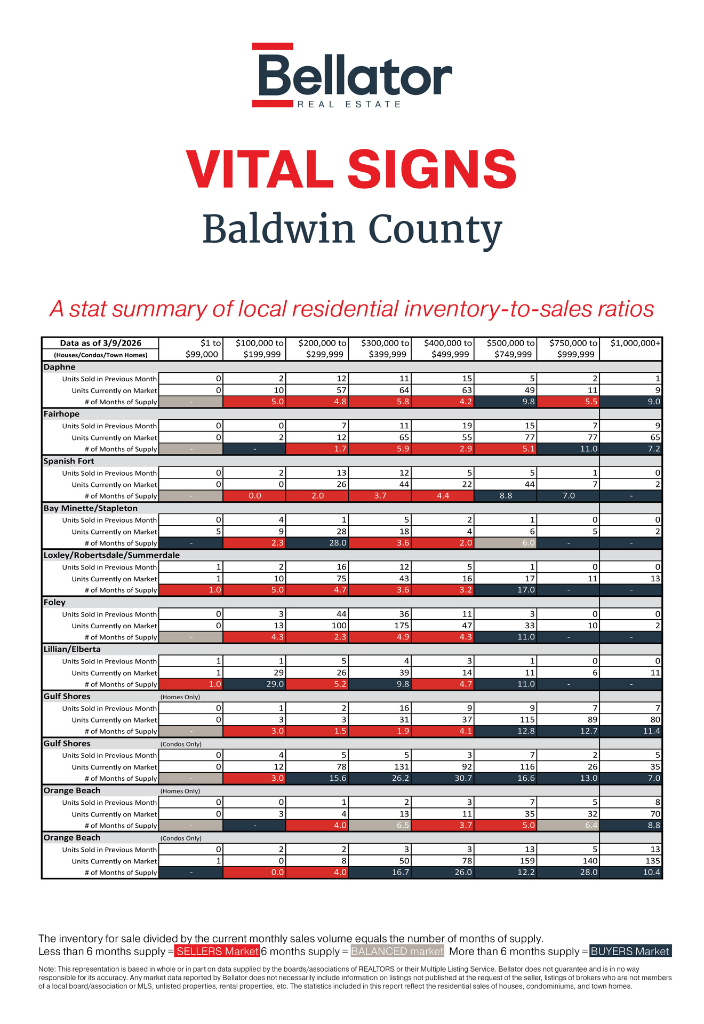

February 2026 Alabama Gulf Coast Real Estate Stats

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

Baldwin County Real Estate Market Update: January vs February 2026

As Baldwin County moved from January into February, the market began showing early signs of the spring buying season awakening. Several areas experienced increased sales activity, particularly in the mid-range price points where demand traditionally concentrates. While inventory remains elevated in certain luxury and coastal segments, many markets saw tightening supply and stronger absorption rates.

Overall, February signals renewed buyer engagement, particularly in the $200,000–$400,000 range across several communities.

Daphne

Daphne showed mixed movement as the market adjusted heading toward spring.

Sales activity between $400,000–$499,999 jumped significantly, rising from 9 sales in January to 15 in February. This surge helped tighten months of supply in that range from 5.9 months to 4.2 months.

Lower price points between $200,000–$399,999 softened slightly, with fewer homes sold and months of supply creeping upward. Meanwhile, higher-end homes above $750,000 saw modest improvement as inventory declined slightly.

Overall, Daphne remains relatively balanced, with strong buyer interest particularly in the upper mid-range price categories.

Fairhope

Fairhope experienced healthy demand growth in February, particularly in the mid-price tiers.

Sales increased in several segments, including:

- $200K–$299K: 5 sales in January to 7 in February

- $400K–$499K: 14 sales to 19 sales

- $500K–$749K: 12 sales to 15 sales

The increased activity significantly tightened inventory in the $400K–$499K segment, reducing months of supply from 4.6 months to just 2.9 months, indicating a competitive market.

Luxury homes above $750K continue to carry higher inventory levels, but steady sales suggest continued interest from higher-end buyers.

Fairhope continues to be one of the most stable and desirable submarkets in Baldwin County.

Spanish Fort

Spanish Fort experienced a notable surge in buyer activity in February.

Sales increased dramatically in the lower and mid-price ranges:

- $200K–$299K: 5 sales to 13 sales

- $300K–$399K: 10 sales to 12 sales

These increases helped tighten months of supply considerably. The $200K–$299K segment dropped from 4.6 months to just 2.0 months, reflecting strong demand.

The $500K–$749K range also improved slightly as sales increased and inventory remained relatively stable.

Spanish Fort is showing strong momentum heading into spring, particularly for move-up and mid-tier buyers.

Bay Minette / Stapleton

This market saw volatile shifts due to smaller sales volume, which can cause dramatic swings in months of supply.

The $200K–$299K segment saw sales drop from 7 to just 1, which caused months of supply to spike significantly. However, other segments improved modestly, particularly the $300K–$399K range where sales increased.

Because inventory levels remain relatively low, this market can swing quickly depending on just a few transactions.

Loxley / Robertsdale / Summerdale

This corridor remained relatively stable month-to-month.

Sales between $300K–$399K doubled from 6 to 12, tightening months of supply from 7.2 months to 3.6 months. Lower price ranges remained steady with moderate inventory increases.

However, homes between $500K–$749K saw inventory rise while sales slowed, pushing months of supply higher.

Overall, the area remains attractive for buyers seeking affordability and new construction options.

Foley

Foley posted one of the largest increases in sales activity across Baldwin County.

The most notable jump occurred in the $200K–$299K range, where sales rose from 28 homes in January to 44 homes in February. This surge dramatically reduced months of supply from 4.3 months to just 2.3 months, indicating strong buyer demand.

The $400K–$499K segment also improved considerably, tightening from 14.7 months to 4.3 months as sales increased and inventory remained manageable.

Foley continues to attract buyers due to its relative affordability and proximity to the coast.

Lillian / Elberta

The Lillian and Elberta market remained somewhat uneven in February.

While some segments showed improved inventory balance, others experienced limited sales activity, which caused months of supply to fluctuate. Homes between $300K–$399K continue to carry elevated supply, indicating slower buyer absorption in that range.

Still, the lower and mid price ranges remain relatively stable overall.

Gulf Shores (Homes)

The Gulf Shores single-family home market saw significant increases in sales activity.

A couple of ranges to note:

- $300K–$399K: 6 sales to 16

- $750K–$999K: 2 sales to 7

This surge dramatically tightened supply in some segments, with the $300K–$399K range dropping to just 1.9 months of inventory, indicating strong buyer demand.

However, higher price points still carry elevated inventory levels, which is typical for coastal luxury markets.

Gulf Shores (Condos)

The condominium market remained inventory-heavy in several price categories, though activity improved slightly.

The most significant challenge remains in the $300K–$499K ranges, where months of supply climbed to extremely high levels due to rising inventory.

Despite this, some higher-end segments saw improved absorption as sales increased modestly.

Orange Beach (Homes)

Orange Beach homes experienced increased luxury market activity in February.

Sales above $500K increased substantially, particularly between $500K–$749K (0 sales to 7 sales) and $750K–$999K (1 sale to 5 sales). These gains helped tighten months of supply dramatically compared to January.

This suggests buyers may be returning to the luxury coastal home market as spring approaches.

Orange Beach (Condos)

The Orange Beach condo market remained supply-heavy, particularly in the mid and upper price ranges.

While sales increased in several categories, including the luxury segment above $1M (4 sales to 13 sales), inventory growth continues to outpace demand. This has resulted in elevated months of supply across many condo price tiers.

This pattern is typical for resort-driven markets where listings accumulate during the off-season.

Baldwin County Market Takeaway

The January-to-February transition reveals a market gradually shifting out of winter slowdown and toward spring activity.

Several key trends emerged:

- Mid-range homes ($200K–$400K) saw the strongest demand increases

- Foley and Spanish Fort posted some of the largest sales surges

- Coastal markets showed improved luxury home activity

- Condo inventory remains elevated across several beach segments

As we move deeper into the spring season, the key question will be whether buyer demand accelerates enough to absorb the growing inventory, particularly in coastal condo markets and higher price points.

For now, Baldwin County remains active and balanced overall, with strong demand continuing in the price ranges that drive the most local transactions.

Mobile County Market Update: January vs February 2026

As Mobile County moved from January into February, the housing market showed a mix of stabilization and early seasonal movement. Several areas saw increased buyer activity in the mid-price ranges, while others experienced rising inventory and slower absorption. The overall trend suggests the market is beginning to transition out of winter's slower pace, though conditions vary significantly by neighborhood and price point.

Across much of the county, the $200,000–$400,000 range continues to drive most of the buyer demand, while higher-end properties and entry-level homes remain more sensitive to inventory fluctuations.

Midtown Mobile

Midtown saw mixed movement between January and February.

Sales activity increased in the $200K–$299K segment, rising from 5 homes sold in January to 9 in February. This helped reduce months of supply from 13 months down to 7.8 months, indicating stronger buyer engagement in that range.

However, inventory increased across several other price tiers, particularly under $200K and between $300K–$399K, pushing months of supply higher. Midtown continues to show demand, but buyers appear to be carefully selecting well-priced homes rather than broadly absorbing available inventory.

Springhill

Springhill experienced a slight rebound in buyer activity during February.

Sales increased in several higher price ranges:

- $400K–$499K saw new activity, with two homes selling after no sales in January.

- $500K–$699K also strengthened, with sales rising from one to four homes.

This increased activity helped tighten supply at the upper end of the market, though lower price points still carry elevated inventory levels. Overall, Springhill remains a stable but competitive market, with buyers taking a more measured approach to purchasing decisions.

Theodore / Grand Bay

Theodore and Grand Bay continued to see steady demand in the mid-price ranges, though activity slowed slightly from January.

Sales in the $200K–$299K segment declined from 19 homes to 12, which pushed months of supply slightly higher. However, the $300K–$399K range remained relatively balanced, suggesting consistent demand from buyers seeking newer construction and more affordable housing options.

Inventory also rose modestly across several price tiers, indicating that supply may be beginning to build heading into spring.

West Mobile

West Mobile remains one of the highest-volume markets in Mobile County, and February showed strong mid-range activity.

The $200K–$299K segment saw sales increase from 38 to 42 homes, while homes between $300K–$399K rose slightly from 26 to 29 sales. These increases helped tighten months of supply in those ranges despite stable inventory levels.

At the same time, higher price ranges experienced slower movement, particularly between $500K–$699K, where inventory remained steady, but sales dropped. Overall, West Mobile continues to be a core driver of the county's housing activity.

Semmes

Semmes posted one of the stronger improvements in buyer activity during February.

Sales in the $200K–$299K range more than doubled, jumping from 8 homes in January to 17 in February. This dramatically reduced months of supply from 7.3 months down to just 3.5 months, signaling a tightening market.

Homes between $300K–$399K also improved, with months of supply dropping below three months, indicating strong buyer demand relative to available inventory.

Semmes continues to attract buyers seeking larger lots and affordability compared to more central areas of Mobile.

Saraland

Saraland remained relatively steady month-to-month.

Sales activity stayed moderate in the $200K–$299K range, while homes between $300K–$399K saw a slight increase in sales compared to January. Inventory levels rose slightly in several categories, which resulted in higher months of supply in some segments.

Overall, Saraland remains a stable submarket, supported by school-district demand and limited inventory.

Dauphin Island

Dauphin Island showed improved sales activity in several coastal price points.

Sales increased in the $300K–$399K range, while the $500K–$699K segment saw a noticeable jump with five homes sold in February. This activity helped bring months of supply down significantly in those ranges.

However, inventory remains elevated in several price categories, which is typical for seasonal coastal markets during the early part of the year.

Mobile County Market Takeaway

The shift from January to February shows a market that is gradually gaining momentum but still balancing rising inventory with selective buyer demand.

Several trends stood out across Mobile County:

- Mid-range homes ($200K–$400K) continue to see the strongest demand

- West Mobile and Semmes posted notable increases in sales activity

- Luxury segments remain more inventory-heavy and slower moving

- Some entry-level markets are still working through elevated supply

As the spring buying season approaches, the key factor to watch will be whether increased buyer activity can keep pace with the growing number of listings coming onto the market.

For now, Mobile County remains a balanced market overall, with strong activity in its most affordable and mid-range price segments.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.